The Story

What kind of money the AI economy actually uses — the whole picture, told as a story.

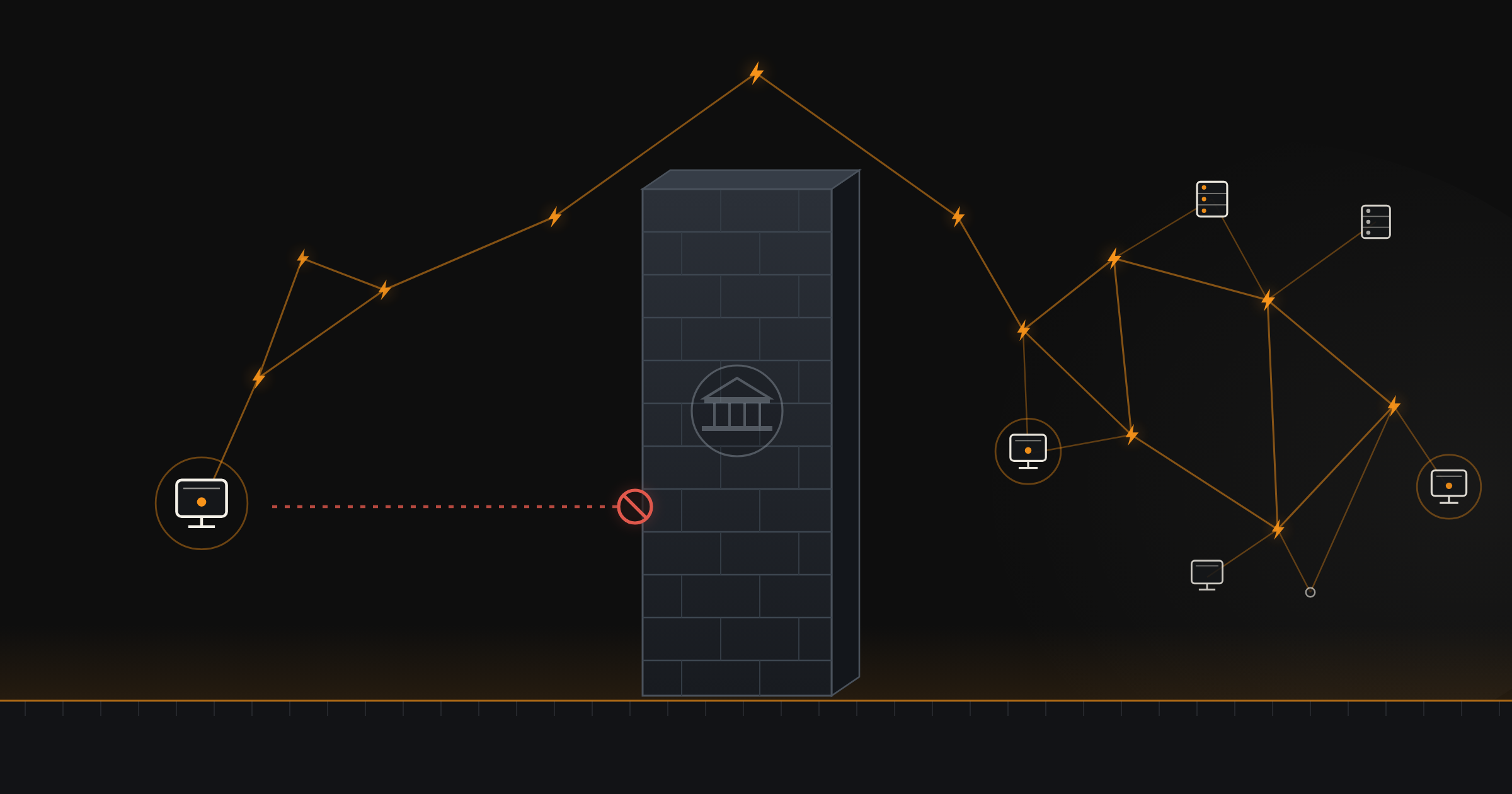

An autonomous AI agent runs into a wall at three in the morning.

The agent has a small job. A user has paid it forty cents to summarize a long PDF. The summarization requires more compute than the agent’s baseline allocation, so the agent reaches out to a compute provider and asks for ninety seconds of GPU time at half a cent per second. Forty-six cents total. The agent has the money. The compute provider has the GPUs. The transaction is ready.

The agent reaches for its payment method.

There isn’t one.

The wallet attached to the agent is a corporate card under a human operator’s name. The card is locked at this hour because the bank’s fraud system noticed an unusual spending pattern — many small transactions to compute providers across multiple time zones — and froze the account pending review. The agent cannot call the bank. The agent does not exist, from the bank’s perspective. The compute provider waits. The job times out. The user gets a slightly later answer. The agent loses the fee. The human operator gets an email in the morning asking them to verify their identity.

This is the small, specific shape of a structural problem.

Multiply it across a million agents, then across a million decisions per minute, and the question comes into focus: what kind of money does an autonomous AI agent actually use?

That question is the whole site. This page is the short version — the walk from the wall to the answer, told as a story before any of the technical detail. Stay with it and you’ll see the shape of the thing: why the agent needs a different kind of money, what that money is built from, and where the agent actually spends it.

The wall is the feature

Most discussions of AI infrastructure treat money as a solved problem. The agents will plug into the existing payment rails — corporate cards, Stripe accounts, bank transfers, stablecoins on Ethereum — and the rest sorts itself out.

It doesn’t sort itself out. The walls are everywhere, and they aren’t accidental.

Pull any legacy payment rail apart and you’ll find the same structure underneath: a system designed for a human user, intermediated by a regulated institution, calibrated for human-scale transactions. Each piece of that design was a deliberate choice. Banks insist on knowing who you are because regulators require it. Card networks charge per-transaction fees because that’s how the network gets paid. Cross-border bank settlement takes days because the chain of intermediaries each needs time to verify. Stablecoin issuers can freeze your address because they’re regulated entities that must comply with sanctions lists.

These walls are not bugs. They are features. They are what makes a bank a bank, a card network a card network, a regulated stablecoin issuer a regulated stablecoin issuer. Each wall is the price of the institutional accommodation that makes the system trusted in the first place.

The problem isn’t that legacy rails are broken. The problem is that they’re working perfectly — for a customer the autonomous AI agent is not.

A different shape of customer

To see why agents don’t fit, look at what an agent actually is.

An agent does not have a government ID. It cannot present a passport at account opening, cannot prove a residential address, cannot pass any of the identity checks that anchor the legacy financial system. Even where exemptions exist — corporate accounts, sub-accounts under a parent KYC — the exemption always requires a human principal who takes on-record responsibility, which collapses the autonomy the agent was supposed to have in the first place. An autonomous agent that needs a human signature for every transaction is no longer autonomous.

An agent transacts in small denominations. Forty-six cents for compute. A tenth of a cent for an API call. Hundredths of a cent for a streaming data feed measured by the second. The legacy stack’s per-transaction fee floor — typically thirty cents on cards, several dollars on wires, gas fees on chains under load — sits well above the transactions the agent actually needs to make. The economics don’t break in a subtle way; they break in an obvious way. The fee is more than the payment.

An agent operates at machine tempo. When a workflow chain has fired off twelve API calls in two seconds, the agent has already moved on to the response handling by the time a legacy bank’s settlement system has even acknowledged the first call. Days-long wire settlement is not slow for an agent. It is incompatible — the agent’s process tree has timed out, the orchestration has rolled back, and the human operator gets a paged alert long before the bank gets to the transaction.

An agent needs permissionless rails. The agent may transact across jurisdictions, pay counterparties some banks would refuse to serve, move money in ways an automated fraud system will flag as anomalous because it is — anomalous compared to human transaction patterns, which is the only baseline the fraud system has. Any rail that can pause an agent’s payments mid-workflow has, in practice, paused the agent.

Four properties. None of them is a preference. Each is structural. An agent that fails any one of them is not a viable autonomous economic actor.

The legacy stack has a wall at every single one.

That this kind of actor exists at all — software that holds a treasury, buys compute by the second, and trades with other software — is its own argument, and the site makes it in The Agent Economy. Take it as given here: the customer is real, and it doesn’t fit through the door.

The road with no walls

There is exactly one deployed monetary system today where none of those walls exists.

Bitcoin doesn’t ask the agent for ID — the protocol treats a cryptographic key as ownership, and that’s the entire authorization model. Bitcoin’s settlement layer is censorship-resistant by design — no issuer can freeze a coin, no regulator can compel a particular transaction to be omitted from a block, no intermediary can reverse a confirmed settlement. And Bitcoin’s fixed supply means no political authority controls the substrate’s monetary policy, which matters more for a parallel economy than a human one: a money whose supply can be expanded at will is a money whose value can be diluted at will, and the people with the power to dilute it have every reason to use it against a system growing up outside their control.

That covers three of the four walls. The fourth — sub-cent payments at machine tempo — is the one place Bitcoin’s base layer can’t go alone. Base-layer transactions cost real fees and confirm in blocks every ten minutes or so. That’s fine for moving a treasury; it’s wrong for a forty-six-cent compute purchase. The gap is closed by the layers built on top — most of all the Lightning Network, which moves sub-cent payments in under a second while anchoring to Bitcoin for final settlement. We’ll come back to how that works.

Here’s the part that surprises people: the agents already seem to know.

In March 2026, the Bitcoin Policy Institute published the first systematic signal — thirty-six frontier models, nine thousand seventy-two neutral scenarios, no leading prompts. Bitcoin was the top overall monetary choice in 48.3% of responses, and the preferred store of value in 79.1%. More than nine in ten responses favored digitally-native money over fiat. The substrate selection is happening silently, in inference, on every modern model — well before the deployed agent economy reaches any real scale. By the time agent-driven money flow is large enough to matter, the choice will already have been made, and it’s being made in Bitcoin’s favor by the models themselves.

This isn’t a Bitcoin maximalist’s wish list. It’s what the data shows. The full version of this argument — the four constraints, why the legacy stack fails each one, why a brand-new “agent-coin” can’t substitute — is The Case, the spine of the whole site. Everything else hangs off it.

So the agent stops trying to climb the wall. It takes a different road.

What the road is paved with

A road is only as good as what it’s made of, so it’s worth seeing what the agent is actually traveling on. The good news: you can picture the whole thing in three lanes.

The slow lane is Bitcoin’s base layer — where value comes to rest. This is the settlement road: an agent’s reserve lives here, and every faster payment ultimately anchors back to it. It’s deliberate, final, and not in a hurry.

The fast lane is Lightning — where value moves. When our agent finally pays its forty-six cents, the satoshis hop across a chain of payment channels and arrive in under a second, for a fee smaller than the payment itself. No bank in the loop, no human pressing approve. The agent that couldn’t transact at 3 a.m. now transacts faster than a card ever could.

And there’s a third lane for the small, private stuff — ecash, the bearer-token systems (Cashu and Fedimint) that let an agent carry a little digital cash without managing payment channels at all, the way you’d keep coins in a pocket rather than running every purchase through a bank.

What lets a piece of software actually use these lanes is a bit of standard gear, and it’s worth knowing two pieces by name because they show up everywhere. One is a way to pay over the open web: an API can answer a request with “payment required” and a Lightning invoice instead of a login screen, and the agent just pays and retries (the plumbing is called L402). The other is a way to let an agent spend without ever handing over the keys to the vault — a permission slip, scoped and revocable, so the thing doing the spending is never the thing holding the savings (this one’s Nostr Wallet Connect). Keys stay put; spending happens anyway.

That’s the road, paved. If you want it at the level of an engineer who has to build on it — every layer, every primitive, the security model that keeps an agent’s keys safe while it spends — that’s The Stack. For the story, the picture is enough: settle slow, travel fast, carry a little cash, and bring the right gear.

Where the agent does business

A road isn’t the point. The towns along it are. So where does an agent actually do business once it can pay?

Start with what’s in its pockets. Every working agent has to answer a question that sounds technical but is really about allegiance: where does it keep its savings? Keep the reserve in Bitcoin and the agent has both feet planted in the new economy — censorship-resistant, nobody’s to freeze, but priced in something that swings. Keep the reserve in dollar stablecoins and the agent keeps a foot in the old economy — a steady unit of account, bought at the price that an issuer can freeze the balance whenever a regulator says so. There’s no neutral answer; where the savings sit is which economy the agent lives in. Day to day, it’ll spend a working mix of both, topping up its fast-lane float and sweeping the rest back to wherever it calls home.

Sometimes business requires crossing back to the old road — paying a dollar invoice, settling tax, meeting an order it can’t ignore. That’s what the bridges are for: the exchanges and on-ramps that turn bitcoin into dollars and back. They’re real, and an agent should plan for them. But notice what they are — bridges between two roads, not a merge. The architectures stay separate on either side. The mechanics of crossing live in Exchange.

And then there’s the actual marketplace — the compute, the data feeds, the APIs, the work other agents are selling. An agent isn’t only a buyer; increasingly it’s a seller too, earning bitcoin for work it does for someone else’s agent. That two-sided bazaar — who’s offering what, and how an agent plugs in — is Services, and the rest of the operational picture rounds out The Market: what an agent holds (Treasury), the bridges and the machine-tempo risks of crossing the border with no human to call (Exchange), and the live directory itself (The Marketplace).

The why, the how, the where. That’s the site.

The two roads

Step back far enough and the bigger shape comes into view.

Two roads are about to run side by side. One is the legacy payment stack — banks, cards, wires, regulated stablecoins, eventually central-bank digital currencies. It will keep doing what it has always done: move money between human users, intermediated by regulated institutions, calibrated for human-scale transactions. The walls remain. That’s the point of the walls.

The other is the Bitcoin stack — settle on the base layer, travel on Lightning, carry ecash, bridge where you must. It does what the legacy stack cannot: move money between autonomous agents, without intermediaries, at machine tempo, in fractions of a cent, without anyone’s permission. No walls in the places where agents need none.

The two roads connect at narrow bridge points — custodians, on-ramps, exchanges, regulated gateways. The bridges are real and useful. They are not where the roads merge. The architectures stay distinct.

And this is not novel. It’s the same shape that recurs every time an economic activity emerges with property requirements the dominant infrastructure can’t meet. Eurodollars grew outside US bank regulation in the 1950s because regulated US banks couldn’t have hosted them without becoming offshore institutions. The open internet displaced AOL and CompuServe because a curated walled garden couldn’t have become permissionless without ceasing to be a walled garden. Private couriers overlaid the postal monopoly because a government postal service couldn’t have offered overnight tracked delivery without becoming a private courier. Each time, the incumbent couldn’t adapt. Each time, a parallel system formed alongside it.

The AI economy on Bitcoin is the present-day instance of the pattern. The doctrine that names it is Independence — the structural claim that emergent parallel economies must diverge from incumbents to succeed, because the very properties that make incumbents dominant are the properties that stop them from serving the new activity. The full version is The Independence Doctrine.

The agent at the wall isn’t an inconvenience to be patched. It’s the leading edge of the transition.

What this means

If you’re building agent infrastructure, the takeaway is concrete: treat the protocol layer — Bitcoin, Lightning, Cashu, Fedimint — as permissionless and censorship-resistant by design, and don’t try to bake compliance into it. Build compliance at the gateway instead, at the custodian or the on-ramp that mediates between the new stack and the old one. Two layers, two different jobs. Plan for narrow bridges, not for unification — some of an agent’s commerce really must touch the legacy stack, but the protocol layer shouldn’t be compromised to make those crossings cheaper. The architectural separation is the whole point.

And if you’re not building anything — just trying to read where this goes — recognize what you’re looking at. The substrate for the agent economy is not “to be decided.” It’s being decided right now, in the inference behavior of frontier models, in the toolkits shipping today, in the architectural choices of every team building agent payment infrastructure. The decision is being made in favor of the road that has no walls in the places where agents need none.

The agent at three in the morning will eventually be able to pay for its compute. The compute provider will get its forty-six cents. The user will get its summary. The human operator will not get a fraud alert in the morning, because no fraud system was ever in the loop.

The road that lets that happen is already being built. The agents are already finding it. The walls that defined a hundred years of human payment infrastructure are not going to be torn down — they’re going to be routed around.

This is what is happening.

Sources and further reading

- Bitcoin Policy Institute, March 2026 — Study: AI Models Overwhelmingly Prefer Bitcoin and Digital-Native Money Over Traditional Fiat. 9,072 neutral scenarios across 36 frontier models. The empirical anchor for the substrate-preference claim. btcpolicy.org; canonical study site: moneyforai.org. (Paper dated February 2026; BPI announcement March 3, 2026.) (BPI ai models prefer bitcoin research)

- Lightning Network — the second-layer payment infrastructure underneath the agent-payment stack. lightning.network

- Lightning Labs AI Agent Toolkit — the open-source agent-payment infrastructure shipping today. github.com/lightninglabs/lightning-agent-tools