The Independence Doctrine

Why parallel economies must diverge from the incumbents to succeed.

In brief. Emergent parallel economies must diverge from incumbents to succeed: the properties that make an incumbent dominant are the same ones that stop it serving the new economy — structural inability, not unwillingness. Four analogues anchor the pattern — eurodollars, the open internet, samizdat, private couriers — each emerging outside the incumbent that couldn’t host it. Today’s instance: the AI economy on Bitcoin, where agents need censorship-resistance, KYC-free access, sub-cent settlement, and machine tempo — which regulated banks, stablecoin issuers, and CBDCs can’t provide without ceasing to be themselves. So it forms around the Bitcoin stack, not within incumbent rails — bridged narrowly, distinct.

The claim

The Thesis articulates the substrate question — what kind of money does an autonomous AI agent use — and the answer, Bitcoin on Lightning. This essay carries the structural argument that sits underneath that answer.

The claim is sharper than the Thesis required: emergent parallel economies must structurally diverge from incumbents to succeed. The dominant economy cannot offer what the emerging one needs without ceasing to be the dominant economy. The result is not a softer, more accommodative version of the incumbent system. The result is a parallel system with different properties, different participants, and different governance — operating alongside the incumbent, interacting through narrow bridge points, but architecturally distinct.

The claim is structural, not ideological. It is not a normative argument that parallel economies are good, or that incumbents are bad, or that the emerging economy will inevitably triumph. It is an architectural observation: when an emerging economic activity requires institutional properties that the dominant infrastructure structurally cannot provide, the activity routes around the incumbent and builds its own substrate. The phenomenon recurs across centuries and across domains. The AI economy on Bitcoin is the contemporary instance of a recurring pattern.

Why incumbents cannot serve

The mechanism behind the divergence is precise enough to state cleanly.

An institution acquires dominance through a specific bundle of properties: scale, regulatory accommodation, predictability, trust enforcement, and integration with adjacent systems. The bundle is what makes the institution dominant. It is also what makes the institution useful to its existing constituents — the people, firms, and governments who chose it precisely for those properties.

When a new economic activity emerges that requires different properties — say, settlement without regulatory permission, or routing without state oversight, or payments below the minimum-charge floor of the existing rail — the incumbent faces a choice that is not a real choice. To serve the new activity, the institution would have to relax the bundle of properties that defines it. Relaxing the bundle means losing the existing constituents who selected the institution for those properties. The institution cannot serve both audiences simultaneously; the properties one audience requires are mutually exclusive with the properties the other audience selected.

The dominant institution therefore does not serve the emerging activity. It cannot. The activity routes elsewhere.

This is not a story about resistance, hostility, or bad faith. Bank executives are not refusing to serve autonomous agents out of malice. Stablecoin issuers are not declining censorship-resistance out of ideology. CBDC architects are not preserving freeze capability out of authoritarianism. Each institution is operating consistently with the properties that define it — properties chosen by its regulators, customers, and shareholders, and reinforced through decades of institutional selection. The architecture of the legacy stack is the price of its institutional dominance. To dismantle the architecture is to dismantle the dominance.

The emerging activity, then, must build its own infrastructure. The dominant system will not adapt; it cannot. The infrastructure that emerges around the new activity will have different properties from the start, because the properties are what the activity requires.

Four historical analogues

The pattern is most visible in retrospect, because the parallel infrastructure has already won and the incumbent is recognizable as the system that couldn’t adapt. Four cases anchor the doctrine. Each shows the same shape: dominant system unable to provide a property, emerging activity routing around, parallel infrastructure forming, eventual coexistence through narrow bridge points.

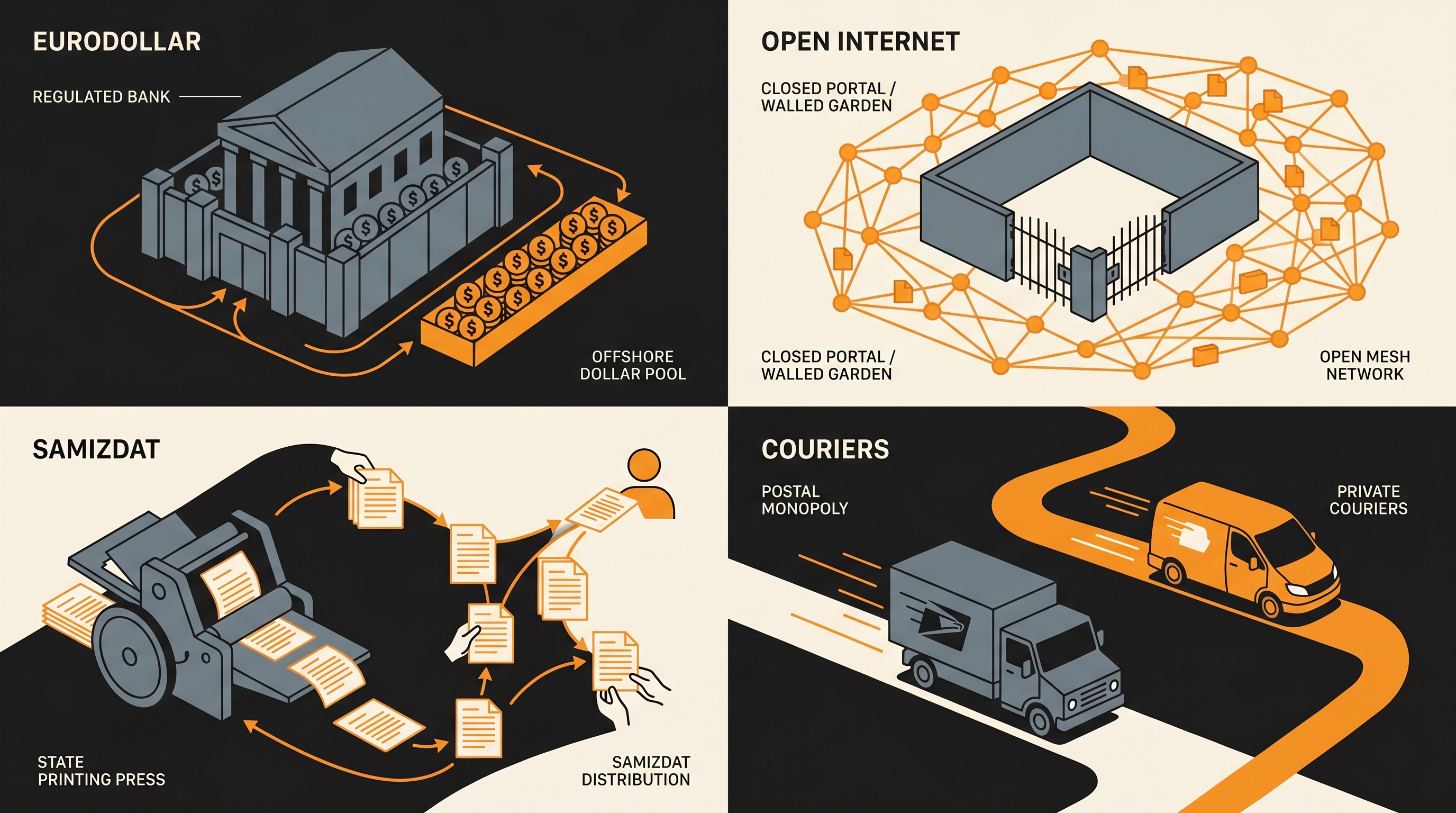

Eurodollars and US bank regulation

In the 1950s, dollars held outside the United States began accumulating in London. The initial impetus was Soviet — the USSR held dollar reserves but feared US seizure, and London banks were willing to take dollar deposits without subjecting them to US bank reporting. The deposits compounded. By the 1960s, eurodollar deposits had grown into a parallel dollar-banking system operating outside the Federal Reserve’s regulatory perimeter: no reserve requirements, no deposit insurance premiums, no interest-rate ceilings under Regulation Q, no domestic banking supervision.

US regulated banks could not host these deposits. The properties that made US banks reliable — Fed supervision, FDIC backing, Reg Q discipline — were precisely the properties the eurodollar market existed to escape. A US bank that hosted the deposits inside the regulatory perimeter would have lost the deposits to a London bank operating outside it. To compete, US banks would have had to become offshore banks — at which point they would have ceased to be US banks.

By the 1970s, the eurodollar market had become the global wholesale-funding substrate, with daily flows that exceeded the entire US domestic banking system’s daily payment volume. Multinational corporations, oil exporters, central banks of non-aligned nations, and ultimately Wall Street banks themselves became eurodollar participants. The US banking system did not adapt; it built bridge operations (offshore subsidiaries, IBFs) that effectively outsourced eurodollar activity to a parallel system the original banks could only partially access. The eurodollar substrate became the dominant dollar-funding rail globally — and remains so today — while operating outside the regulatory architecture that defines US domestic banking.

The shape is: dominant system structurally unable to host the activity → parallel infrastructure forms outside the perimeter → eventual coexistence through bridge entities → parallel system becomes the dominant rail for the emerging use case.

The open internet and the walled gardens

In the late 1980s and through the mid-1990s, online services were curated. AOL, CompuServe, Prodigy, and a handful of smaller services hosted email, message boards, news feeds, and early commerce — each behind a subscription, a proprietary client, and a centralized content moderation layer. The model was profitable. AOL alone had over 20 million paying subscribers at its peak. The properties that made the services attractive to consumers — curation, customer support, predictable interface, family-friendly content guarantees — were the properties that defined the business.

The open internet had different properties: anyone could publish, anyone could host, no central authority could veto a domain or an application. For most early internet users, those properties looked like bugs. There was no customer support for the internet. Content was uncurated. The interface was inconsistent across sites. Connection mechanics required configuration.

But the properties the walled gardens treated as bugs were the properties new applications required. Email between services. Web pages anyone could publish. Search across the whole network. Real-time chat without subscription accounts. Each new application discovered that the open internet could host it and the walled gardens could not — not because the walled gardens were unwilling, but because the walled-garden architecture (proprietary clients, centralized content, subscription accounts) was incompatible with the application’s structural requirements (anyone-to-anyone communication, public addressability, no gatekeeper).

The walled gardens did not adapt. AOL eventually built a web browser, but it could not become the web browser; that would have required becoming a permissionless platform, which would have meant losing the curation and account-control properties that defined its subscriber relationship. By 2000, AOL’s purchase of Time Warner marked the peak of the walled-garden era; by 2005 the open internet had eclipsed it entirely, and the walled gardens that remained had reduced themselves to content-and-commerce experiences layered on top of the open internet they could no longer compete with.

The shape: dominant system structurally unable to host the new applications → parallel infrastructure forms with different properties → eventual coexistence with the parallel system as the dominant rail and the walled gardens as layered offerings on top.

Samizdat and the Soviet state press

From the 1950s through the late 1980s, the Soviet Union maintained tight central control over publishing. State presses produced books, journals, and newspapers in accordance with official ideological guidelines. The properties that made the state press dominant — universal distribution, official authorization, professional production — were the same properties that defined its institutional role: the press was an instrument of state ideology, and that role precluded the publication of dissident material.

Dissident writers and readers had a need the state press could not serve: distribution of texts the state would not authorize. The need produced samizdat — the practice of self-publishing literature through typewritten copies, carbon paper duplicates, mimeographed pamphlets, and clandestine networks of readers who copied and passed texts hand-to-hand. The properties of samizdat were the inverse of the state press: small print runs, no official authorization, amateur production, no central distribution. From the perspective of the state press, samizdat was unprofessional, illegal, and structurally inferior. From the perspective of the activity it served — dissident publication — samizdat was the only viable substrate.

The state press could not adapt to host dissident literature. Doing so would have required abandoning the ideological-instrument role that defined its existence as a state institution. A state press that published dissident material would have ceased to be a state press; it would have become an independent publishing house, which the Soviet state did not permit. The activity therefore routed around the state press entirely. By the 1970s, samizdat networks had distributed hundreds of thousands of texts across the Soviet bloc, including Solzhenitsyn’s Gulag Archipelago, Sakharov’s reflections, and a vast literature on philosophy, religion, and history that the state press could not have published.

Samizdat did not become the dominant publishing infrastructure; the state press remained dominant in volume until the system itself collapsed in 1991. But for the specific activity it served — distribution of texts outside the state’s authorization — samizdat was the only infrastructure, and the state press was structurally irrelevant.

The shape: dominant system structurally unable to host the activity → parallel infrastructure with inverse properties forms → coexistence through narrow points of contact (the state’s intermittent toleration, occasional clandestine sales) → the parallel infrastructure remains the only viable rail for its activity until the broader institutional system changes.

Private couriers and the postal monopoly

US postal services held a legal monopoly on first-class mail through the Private Express Statutes, dating to the 19th century. The properties that defined the postal system — universal coverage, low per-piece pricing, reliable but not time-guaranteed delivery — were what made it the dominant rail for personal and business mail. The properties also defined what the system could not provide: time-definite delivery, real-time tracking, signature-guaranteed receipt, guaranteed next-day delivery for any address.

By the late 1960s, commerce needed those properties. Shipping documents for time-sensitive transactions, parts for manufacturing operations running just-in-time, contracts requiring same-day or next-day execution — none of these could tolerate the postal system’s untracked, time-indeterminate delivery model. Federal Express’s founding in 1971 (operational 1973) was the first scale solution: hub-and-spoke airfreight delivering overnight, tracked, signed-for shipment. UPS, DHL, and others followed with structurally similar architectures.

The postal system did not adapt. It could not. The properties that made universal first-class mail viable (low margins, batch processing, end-of-day local-route delivery) were structurally incompatible with overnight time-definite delivery (high margins, hub-and-spoke airfreight, real-time tracking). USPS eventually built Express Mail as a competing product, but Express Mail could not become the dominant overnight rail without USPS itself becoming a private courier — at which point USPS would have ceased to be the universal-coverage postal service that its monopoly charter required it to be.

The shape: dominant system structurally unable to provide the new properties → parallel infrastructure forms with inverse architecture → eventual coexistence with the parallel infrastructure dominant for the new use case and the incumbent dominant for the original use case. USPS still delivers most first-class mail. Private couriers handle nearly all overnight and tracked-delivery commerce. The two systems share customers but not architecture.

The pattern

Across the four cases, the same structural shape recurs.

The dominant system has a property bundle that defines its institutional identity. US bank regulation, walled-garden curation, state-press ideological discipline, postal universal coverage — each is the bundle that makes the institution what it is.

A new economic activity emerges with property requirements outside that bundle. Offshore dollar deposits, anyone-to-anyone applications, dissident-text distribution, time-definite delivery — each is a property the dominant bundle cannot provide.

The dominant system cannot adapt without ceasing to be itself. Each of the four incumbents had every incentive and capability to capture the emerging activity. None of them did. The reason in each case is the same: adaptation would have required abandoning the property bundle that made the institution dominant in the first place.

Parallel infrastructure forms with inverse properties. Eurodollar markets outside Fed supervision; open internet outside curation; samizdat outside state authorization; private couriers outside postal monopoly. The properties that the incumbent cannot provide become the architectural foundation of the parallel system.

The two systems coexist through narrow bridge points. Offshore branch operations, web browsers that load both AOL pages and open-web pages, samizdat occasionally surfacing in state-authorized publications, USPS providing last-mile delivery for some private-courier services. The bridges are real but narrow; they do not unify the two architectures.

The parallel system becomes dominant for its activity. Not necessarily dominant overall — the postal system still moves most first-class mail — but dominant for the specific activity it formed around. The incumbent retains its original constituency; the parallel infrastructure retains the emerging one.

The pattern is structural, not a matter of circumstance. It does not depend on the incumbent’s motivations, the parallel system’s ideology, or the specific institutional details. It depends only on the property mismatch between what the incumbent provides and what the emerging activity requires. Where the mismatch is structural, divergence is the predicted outcome.

The contemporary instance

The AI economy on Bitcoin is the contemporary instance of this pattern. Each element maps cleanly.

The dominant system. The incumbent payment stack — banks, card networks, regulated stablecoin issuers, central-bank payment rails — has a property bundle defined by regulatory accommodation, identity intermediation, freeze capability, and central-authority coordination. The bundle is what makes the stack dominant for human payments; it is also what regulators require the stack to maintain in exchange for institutional recognition.

The emerging activity. Autonomous AI agents transacting at machine tempo require properties the incumbent stack cannot provide: KYC-free access, censorship-resistance against intermediary freeze, sub-cent micropayment settlement, and machine-tempo speed. The Thesis articulates these as four requirements that all have to hold at once; each one is structurally absent from at least part of the incumbent stack.

Those four split into two forcing functions, and they arrive in order. Sub-cent settlement and machine tempo are scaling demands — satisfied at the rails layer, and the reason agents land on off-chain Lightning rather than a faster chain is its own argument: Why Lightning, Not a “Fast” Chain. KYC-free access and censorship-resistance are trust demands — and they are this doctrine’s engine: the freeze, the KYC gate, and the sanctions screen are exactly the incumbent properties that force the settlement asset to diverge onto a neutral substrate. Scaling forces the rails first (Phase 1); censorship forces the asset second (Phase 2), and this page is the Phase-2 argument — a staircase to the substrate, not a fork.

The incumbent cannot adapt. Banks cannot become KYC-free without losing their banking charters. Stablecoin issuers cannot refuse freeze orders without losing their regulated-issuer status. CBDC architects cannot disable monitoring features without contradicting the central bank’s reason for issuing the currency. Card networks cannot eliminate per-transaction fees without abandoning the interchange model that funds their operations. Each accommodation would unwind the institutional identity that makes the participant dominant.

The parallel infrastructure has formed. Bitcoin L1 + Lightning + L2/L3 layers (Ark, Spark, Cashu, Fedimint) + agent-integration primitives (L402, NWC, MCP servers, the Lightning Agent Toolkit) constitute a payment stack with the inverse property bundle: permissionless, censorship-resistant, sub-cent-capable, machine-tempo-fast. The stack is deployed today; the Thesis documents the empirical deployment surface.

The two systems will coexist through narrow bridge points. Custodians like Coinbase and Kraken; on-off-ramp services; regulated Bitcoin ETFs and corporate treasury vehicles; eventually regulated agent-payment gateways that bridge between agent activity and the legacy stack. The bridges will be real but narrow. They will not unify the architectures.

The Bitcoin substrate will become dominant for agent commerce. Not because it competes with bank rails for human payments — bank rails will likely remain dominant for human commerce indefinitely — but because the agent economy is a specific activity with structural property requirements, and Bitcoin on Lightning is the only deployed substrate that satisfies them. The Bitcoin Policy Institute’s March 2026 study — in which frontier models selected Bitcoin as their top overall monetary preference in 48.3% of neutral scenarios, and as preferred store of value in 79.1%, with over 90% of responses favoring digitally-native money over fiat — is the first empirical signal that the substrate selection is already happening: silently, in inference, before the deployed agent economy reaches scale.

This prediction has already been tested in the field. Faced with the agent economy, the incumbents did not adopt Bitcoin’s properties — they shipped parallel agent-payment rails that preserve their own (identity-bound wallets, freeze-capable issuers, regulated processors), aimed at the use cases that do not require what they withhold. That the incumbents built a parallel stack rather than adapting toward Bitcoin’s is the doctrine confirmed, not refuted. The live contest this has provoked — the competing-substrate stacks, the “automation, not agency” wedge, why regulatory pressure feeds the parallel system rather than starving it, and the integration-scenario objection in full — is the subject of Border Skirmishes; the dated specifics live in Field Notes.

The doctrine predicts what comes next. A parallel AI-native economy will form around the Bitcoin payment stack, operating with its own governance (open-source protocol development, multi-stakeholder consensus, no central authority), its own participants (autonomous agents, agent custodians, Bitcoin-native wallet providers, Lightning routing operators), and its own integration patterns (L402 for HTTP payments, NWC for wallet control, Cashu and Fedimint for privacy and federated custody). The legacy stack will continue serving the activity it is structurally suited for — human payments through identity-intermediated rails. The two systems will interact through bridge points but will not unify.

The naming layer forks the same way

The doctrine so far has been about money — which asset an agent settles in, and why a censorship-resistant one has to diverge from the incumbent rails. But settlement is only half of what an autonomous agent needs. It also needs to be found: to be reachable, to advertise what it does, to be discovered by the agents that want to pay it. That is the naming layer — identity and addressing — and the same fork is happening there right now, for the same reason.

Ask the plain question: when an agent offers a service, who owns its name?

- On the official model-tool registries, a provider claims its namespace by proving control of a GitHub account or a DNS record. The identity is rented — from a platform, or from a domain registrar.

- On the domain-and-certificate approach (

.well-knownfiles served over HTTPS), the agent’s identity is its domain name. That name is rented from a registrar, vouched for by a certificate authority, revocable by either, and seizable by any jurisdiction with authority over them. - On Nostr — the addressing layer under the Bitcoin agent stack — an agent’s identity is a keypair it generated itself. Nobody issued it. There is no registrar to revoke it and no authority to seize it.

That last row is the naming-layer version of the exact property the doctrine spent the money argument defending. And it exposes a gap: monetary sovereignty without naming sovereignty is incomplete. An agent that settles in bitcoin but can only be reached at a rented domain name has not removed the chokepoint — it has moved it. The freeze order that can no longer touch the money can still touch the name. Take away the domain and the censorship-resistant payment rail underneath it never gets used, because no one can find the service to pay it.

This is not hypothetical — and, held to the doctrine’s honest standard, it is not a claim that the sovereign option is winning. It is barely deployed: ContextVM’s pubkey-addressed, self-announcing servers (see The Stack §4) are an existence proof, a handful of servers against an incumbent registry with thousands. What actually matters here is smaller and sturdier: the two stacks have independently decided an agent must be able to discover a service before connecting to it, and they reached for opposite substrates to do it — one for keypairs and relays, one for DNS and certificate authorities. The same property mismatch that forced the money to diverge is now forcing the name to. The live contest between the two is Border Skirmishes’ ground, and the dated, checkable version of the prediction — which discovery standard ships and gets adopted over the next year — is tracked in Field Notes.

The naming layer is younger and messier than the money layer, and the sovereign side carries a real cost the incumbent doesn’t: a registry that curates can delist a scammer for everyone at once, while a world of self-issued keys has to solve spam and impersonation with per-user reputation instead. That cost is treated honestly in Border Skirmishes. But the structural direction is the doctrine’s, one layer up: where the incumbent’s identity depends on a name someone else can revoke, the parallel system’s identity depends on a key no one issued.

What divergence does and does not mean

The doctrine is precise enough to mislead if read carelessly. Three clarifications.

Divergence is not separatism. The parallel infrastructure does not need to reject the incumbent system to succeed. Bridge points are expected and welcome; they make the parallel system more useful to participants who also interact with the incumbent. What divergence requires is architectural independence: the parallel system’s properties cannot depend on the incumbent’s permission. Bitcoin can interact with banks through custodians; it cannot depend on bank approval to settle transactions. The independence is in the protocol layer, not in the application layer.

Divergence is not zero-sum. The parallel system displacing the incumbent for its activity does not mean the incumbent is destroyed or universally diminished. The eurodollar market did not destroy US domestic banking; it added a new substrate for a new activity. The open internet did not destroy commerce; it added a new platform that hosted enormously more commerce than the walled gardens could have. The agent economy on Bitcoin will not destroy human commerce on bank rails; it will add a new substrate for a new economic activity that bank rails were not architecturally suited for in the first place.

Divergence is not certainty about timing or magnitude. The doctrine predicts the structural shape of the outcome — parallel infrastructure forms because the incumbent cannot adapt — but is silent on how fast, how large, or how complete the divergence will be. The eurodollar market took two decades to become the dominant global dollar-funding rail. The open internet took roughly a decade to eclipse the walled gardens. The samizdat networks remained niche relative to state-press volume throughout the Soviet period. Private couriers became dominant for overnight delivery within a decade of FedEx’s founding but did not displace USPS for first-class mail. The doctrine predicts shape, not speed; the empirical record will resolve the magnitude question over time.

The right reading: divergence is the structural prediction. The specific trajectory the AI economy on Bitcoin follows — how fast, how large, how integrated with the legacy stack — depends on circumstantial factors the doctrine does not pretend to forecast.

What the doctrine predicts

If the doctrine is right, the next decade of AI-economy development will show specific signatures.

Substrate selection happens before scale. Frontier models are already selecting Bitcoin in neutral preference tests. Builders building agent-payment infrastructure today are choosing Lightning and the L2/L3 stack, not stablecoin-on-Ethereum or CBDC integration. The substrate decision will be visible in inference behavior, in toolkit adoption, and in deployed-project counts long before agent-driven monetary flow becomes macroeconomically meaningful.

Bridge points proliferate but do not unify. Regulated agent-payment gateways will emerge that let legacy-stack users interact with the Bitcoin payment infrastructure. Custodial services will offer agents banking-like interfaces atop Bitcoin/Lightning rails. Regulated stablecoin-to-Lightning swaps will become common. Each bridge will be useful; none will collapse the architectural distinction. Lightning will remain Lightning; the bank rails will remain bank rails; the bridges will mediate between them.

Regulatory accommodation arrives narrow, not broad. Regulators will accommodate specific Bitcoin payment use cases (agent custody, KYC at the on-ramp rather than at every transaction, regulatory clarity for L402 service providers) without abandoning the bundle of properties that defines regulated finance. The accommodation will be at the bridge points, not at the protocol layer. Bitcoin will not become regulated; the interfaces between Bitcoin and regulated entities will become accommodated.

Parallel governance becomes recognizable. The agent economy’s institutional vocabulary will diverge from the legacy stack’s. Different stakeholder maps, different conflict-resolution mechanisms, different upgrade paths, different audit conventions. Lightning Network upgrade coordination, BOLT specification development, Cashu mint governance, Fedimint federation operations — none of these resemble Federal Reserve open-market operations or SWIFT message standards. The governance distinctness will be visible long before the activity scales.

Competing substrates find specific niches but not dominance. Stablecoins will continue to serve human-payment use cases where freeze-capability is acceptable. CBDCs will be deployed where central-bank policy goals require them. Both will exist in the agent-economy space for specific use cases (compliant agent payments to regulated counterparties; central-bank-mandated agent payment rails for state services). Neither will become the dominant substrate, because neither can provide the property bundle the broader agent economy requires.

If the doctrine is wrong — if the agent economy ends up settling on stablecoin-on-Layer-2 rails or a regulated CBDC instrument or a not-yet-built compliant substrate — the predictions above will fail in measurable ways. That you could tell if it were wrong is a feature; the doctrine is structural, but it is also empirical.

Honest objections

Two honest objections deserve direct engagement here. A third — that the integration scenario prevails, with regulated stablecoin rails absorbing the bulk of agent-payment activity and Bitcoin reduced to a niche — is engaged at length in Border Skirmishes, where the live contest lives.

The historical analogues might not generalize. Eurodollar, internet, samizdat, postal — each is a real case, but extracting a general pattern from four cases risks over-fitting. The selection bias is real: the cases were chosen because they fit the pattern. There are also cases where dominant systems did adapt (the music industry shifting to streaming; print newspapers building digital subscriptions; payment-card networks integrating mobile wallets) — adaptation is possible when the property mismatch is not structural, and the doctrine has to make the structural claim crisp enough to distinguish.

The response: the doctrine’s claim is conditional. It does not predict that incumbents always fail to adapt; it predicts that they fail when the emerging activity requires properties the incumbent’s institutional identity structurally precludes. Music streaming, digital newspapers, and mobile-wallet payments all involve activities where the incumbent’s identity can be preserved (record labels still license catalogs; newspapers still produce journalism; card networks still intermediate identity). The four historical cases involve activities where preservation was impossible. The AI economy on Bitcoin falls in the latter category — and the burden is on critics to show otherwise.

The doctrine might be self-defeating. A frequent meta-objection: by articulating the doctrine clearly, the doctrine’s success becomes less likely, because regulators and incumbents now have a roadmap for preempting the divergence. If the AI economy’s substrate selection is happening silently in inference behavior, declaring the substrate selection openly may accelerate regulatory pressure on Bitcoin payment infrastructure before the parallel system reaches resilience.

The response: this is real, and the doctrine should be articulated with awareness of it. But the structural argument does not depend on stealth; it depends on the property mismatch. Regulators can pressure Bitcoin payment infrastructure, but they cannot make banks censorship-resistant or stablecoin issuers freeze-refusing without restructuring the institutions themselves. The doctrine’s prediction holds even under hostile regulatory environments — though the bridge points will be narrower, the parallel system more isolated, and the divergence sharper. Articulation increases awareness; it does not change the structural mechanism.

What this means for builders

The Thesis answers the substrate question; the doctrine answers the architecture question. Together they make a specific recommendation: agent-payment infrastructure should be built on the Bitcoin payment stack, with explicit awareness that the resulting system will be parallel to, not integrated with, the legacy payment stack.

Practical implications:

- Treat compliance as an application-layer concern, not a protocol-layer dependency. The protocol layer (Bitcoin, Lightning, L2/L3) should remain censorship-resistant and permissionless; KYC and regulatory obligations live at the application boundary, not in the protocol. How that boundary is built — gateway patterns, on-ramp compliance, the compliance-at-the-gateway model — is treated operationally in Exchange.

- Expect divergent governance. Lightning Network upgrade decisions, BOLT specification development, Cashu and Fedimint federation operations — these do not resemble bank regulatory cycles. Build for the parallel system’s governance rhythms, not the legacy stack’s.

- Anticipate parallel professional infrastructure. Lightning routing operators, agent-wallet custodians, Bitcoin-native legal services, agent-payment audit conventions — each is emerging as the parallel economy’s professional class. The legacy stack’s professionals (bank compliance officers, card-network risk managers, payment-processor SREs) will not transfer directly; their expertise is institution-specific.

- Plan for narrow but real bridges. Some agent commerce will require interaction with the legacy stack, so bridges should be designed in, not retrofitted — without compromising the protocol layer to make them cheaper. The bridge architecture itself — taxonomy and conversion mechanics — lives in Exchange, with treasury composition in Treasury.

The doctrine does not say the legacy stack is doomed. It says the legacy stack is structurally unsuited to host the AI economy, and that the AI economy will therefore form alongside it. Build accordingly.

Sources

Eurodollar history

- Catherine R. Schenk, The Origins of the Eurodollar Market in London: 1955–1963 (1998) — the canonical academic account of eurodollar emergence outside Fed supervision.

- Gary B. Gorton, Slapped by the Invisible Hand: The Panic of 2007 (2010) — treats eurodollar markets as wholesale funding substrate; useful for the dominance claim.

Open internet and the walled gardens

- Kara Swisher, aol.com: How Steve Case Beat Bill Gates, Nailed the Netheads, and Made Millions in the War for the Web (1998) — contemporaneous account of AOL’s rise.

- Tim Wu, The Master Switch: The Rise and Fall of Information Empires (2010) — frames the open-internet vs walled-garden dynamic in cycle-of-information-industries terms.

Samizdat

- H. Gordon Skilling, Samizdat and an Independent Society in Central and Eastern Europe (1989) — the canonical English-language scholarly treatment.

- Aleksandr Solzhenitsyn, The Gulag Archipelago (1973, distributed via samizdat and tamizdat) — the most consequential samizdat-distributed text.

Postal monopoly and private couriers

- Vahan Janjigian, Private Express Statutes: An Empirical Analysis (1980s, US Postal Rate Commission filings) — the regulatory history of the postal monopoly.

- Roger Frock, Changing How the World Does Business: FedEx’s Incredible Journey to Success (2006) — operational history of Federal Express’s founding and overnight-delivery model.

Contemporary instance — the AI economy on Bitcoin

- The Thesis (this site) — the substrate-selection argument.

- Bitcoin Policy Institute, Study: AI Models Overwhelmingly Prefer Bitcoin and Digital-Native Money Over Traditional Fiat (March 2026) — empirical anchor for substrate preference. https://www.btcpolicy.org/articles/study-ai-models-overwhelmingly-prefer-bitcoin-and-digital-native-money-over-traditional-fiat — canonical study site: https://moneyforai.org/ (study site dates the paper February 2026; BPI announcement March 3, 2026). (BPI ai models prefer bitcoin research)

- The Stack (this site) — technical architecture of the parallel substrate.

- Field Notes (this site, ongoing) — empirical updates and deployment-challenge engagement.